Currency-hedged ETFs were extremely popular for much of 2015 as investors sought to win two times over by owning shares from countries such as Japan and Germany (which they expected to do well given a devaluing currency), and also benefit from being short the depreciating currency. However, as many studies have shown, this strategy has been a mixed bag over the very long term as currency movements tend to mean-revert.

Furthermore, for US investors, currency hedging of foreign equity positions can take away a valuable diversification benefit. With help from my friend Jake (@econompic on Twitter), I examined the relative performance of US stocks (using the S&P 500) versus the MSCI EAFE (Europe, Asia, Far East) index during various dollar cycles.

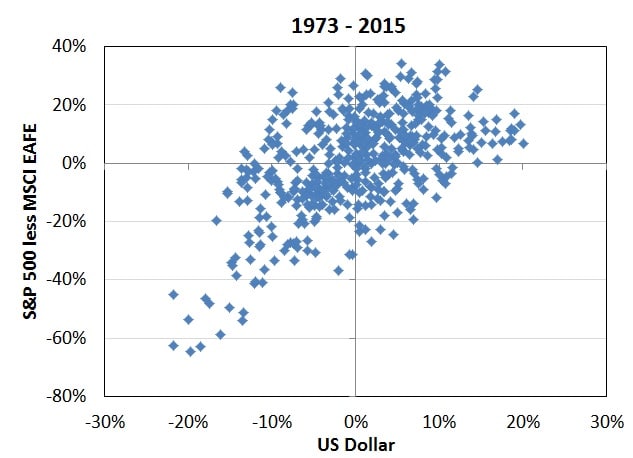

As you can see from Jake’s graph, there has been strong correlation between dollar movements and S&P 500 outperformance/underperformance over the last several decades. In other words, as the USD has declined in value relative to other currencies, US investors benefitted from unhedged foreign equity exposure as the MSCI EAFE has tended to outperform US stocks during down dollar cycles. Conversely, the S&P 500 has outperformed relative to global equities when the dollar has gained against competing currencies:

Finally, I examined the average annual performance of the S&P 500 and the MSCI EAFE during a few of the major USD cycles since the early 1970s (the USD was delinked to gold in 1971):

As you can see from the table above, owning unhedged foreign equities has been a great portfolio diversifier (as well as a great source of returns) during weak dollar periods. Currency-hedged ETFs, I believe, can be popular as a trade, but they are likely to be a poor substitute for the unhedged alternative.