Note: If this post sounds repetitive of arguments I have made before, that is because it is. The goal of this post is to build on those previous arguments by articulating them in slightly more detail with the hope of making them more comprehensive and more cogent.

Emerging market (“EM”) stocks have been among the top performers this year as EM technology shares – now the largest-weighted sector in the MSCI EM index – have propelled the index to its best single-year performance since 2009. Many analysts and commentators feel that the rally in EM shares may be only in its infancy as many valuation metrics such as the cyclically-adjusted price-to-earnings ratio, or “CAPE,” point to a substantial discount for EM stocks versus, for example, U.S. shares.

I confess, however, to being a skeptic, which should come as no surprise to readers familiar with my blog. The reality is that EM investing is extremely difficult as investors used to the relative simplicity of investing in the U.S. must now confront far more variables in the EM space, such as currency volatility and geopolitical uncertainty.

GMO touched on this earlier this year in an article titled, “Revisiting the Traditional Emerging Market Equities Allocation Framework.” GMO noted that even though emerging market investing has been profitable over the last thirty years (the MSCI EM Index started in 1988), it has come at the expense of far greater volatility, and much more frequent and steeper drawdowns. GMO points out that since 1990, each of the countries within the MSCI EM index has fallen at least 20% twenty-two times, while over the same period the S&P 500 has fallen by 20% only four times. GMO sums it up nicely when they say that, “[a]s EM investors, our priority is to ensure return of capital first. Return on capital is step two.”

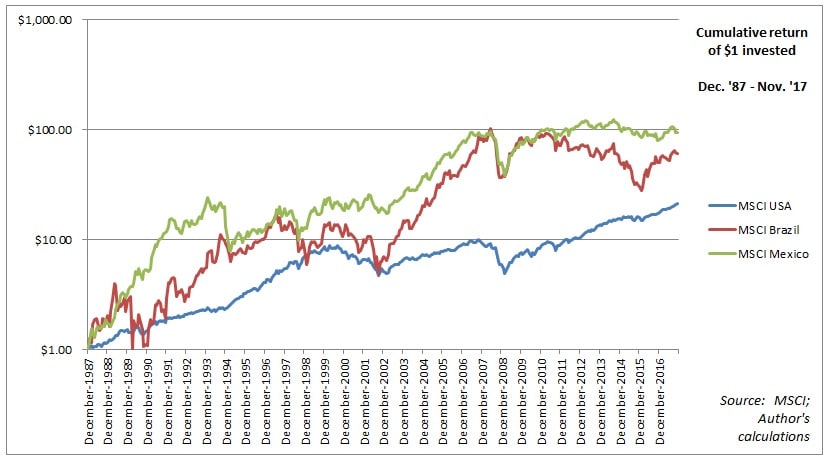

To visualize this volatility, we can take a small sample of the EM universe, Mexico and Brazil. Both the MSCI Mexico and Brazil country indices have return data going back to 1987, and since their inception through November of this year, each has dwarfed the returns from U.S. shares…

…but with much, much more volatility:

Enticed by seemingly bargain-level valuations on the equity markets of select individual EM countries, a few brave investors may even be tempted to eschew investing in EM indices and take concentrated positions in these individual countries. Before doing so, however, investors should consider the following.

Since December of 1994 (the earliest common starting point), twelve of the largest EM markets have outperformed the MSCI index, while ten have lagged:

Several of the countries that outperformed the index such as Brazil, Russia, and the Czech Republic are currently among the ‘cheapest’ markets in the world. If investing were this simple, then it would be safe to assume that one can now buy quality shares at a discount. But, alas, it is not that simple. Most individual emerging market indices are highly concentrated in one sector, which is typically financials. What is more, with the exception of India, the top holding constitutes at least 10% of the market:

In contrast to U.S. equities, which among global equities trade on macro factors the least (thus suggesting a higher degree of market efficiency), this high degree of concentration in EM indices means that single factors such as commodity prices can dictate the direction of the entire market.

For example, 48% of the MSCI Russia index is energy, and so Russian equities follow the price of oil very closely…

…which largely explains why the MSCI Russia index has been in a drawdown since peak oil prices in 2008:

Suffice it to say, then, that investors going long Russian equities are more than anything making a bet on oil prices.

The same story of commodity sensitivity is true for a country like Indonesia, which as a copper producer is heavily exposed to the price of the industrial metal:

This is incomplete analysis, however. After all, developed market Norway is also highly sensitive to the price of oil…

…and, like the Russian market, remains well below its 2008 peak. Yet unlike Russian stocks, Norwegian equities remain much closer to break-even than Russia, which suggest that investors have more confidence in Norwegian equities than Russian equities, even though both move largely in concert with many of the same macro forces:

The same is also true for developed market Australia, a huge copper producer, relative to Indonesia. Both Australian and Indonesian equities track the price of copper very closely, but as with Norway and Russia, the developed market Australia trades closer to break-even:

In reality, as JP Morgan’s Richard Titherington has stated, the term emerging market is a bit of a misnomer, as it implies some kind of inevitable graduation, as it were, of these nations from ’emerging’ to ‘developed.’ The simple truth, remains, however, that these emerging nations are, unfortunately, likely to remain ’emerging’ in the sense that most of them will likely always face the threats of higher levels of inflation and political uncertainty than developed nations, and so even while their economies may grow, their equity markets may remain fairly undeveloped in the sense that they will probably never see the kind of robust diversification across industries that is the hallmark of many developed nations.

That is because many emerging nations face a continuing ‘brain drain.’ Consider, for example, that over the last twenty years, even as these emerging economies have grown and their equity markets have, in most cases, flourished, more individuals left these nations than immigrated to them. The reverse has been the case for developed nations:

What this loss of human capital likely means is that most emerging markets will likely be left with the ‘immobile’ industries such as those associated with commodity extraction, utilities, and local financial corporations, while markets such as those in Japan, Europe, and the United States become increasingly populated with truly global brands and the growing industries of the knowledge economy.

None of this is to say, of course, that emerging markets are to be avoided. On the contrary, they remain a worthwhile building block of any prudently diversified portfolio. However, single country EM investing is perilous, and prudent investors should consider broadly diversified emerging market portfolios as their default choices for exposure to the EM universe. Further, in my view, EM stocks should be seen as diversifying components within a portfolio, not as core (meaning heavily weighted) positions. Finally, those who consider markets such as the U.S. unacceptably ‘expensive’ and the EM universe ‘cheap’ would do well to think carefully before making major allocation shifts based on aggregated valuation metrics alone.