A few months ago, I wrote about the compelling case for pairing minimum volatility with momentum strategies in a “barbell” approach. The idea, in a nutshell, was to create a 50-50 portfolio of Minimum Volatility & Momentum (rebalanced annually). This balancing of two extremes would help limit the extremes experienced by each factor portfolio during certain cycles (think the tech bubble and its aftermath for momentum), making the ride much smoother for investors by reducing long periods of underperformance.

In this post, I will perform the same analysis for overseas markets as defined by MSCI’s “EAFE” Index (Europe, Australasia, and Far East) for foreign developed, and MSCI’s Emerging Markets index to see if the idea shows merit in non-US markets.

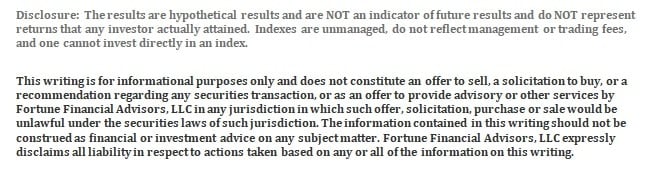

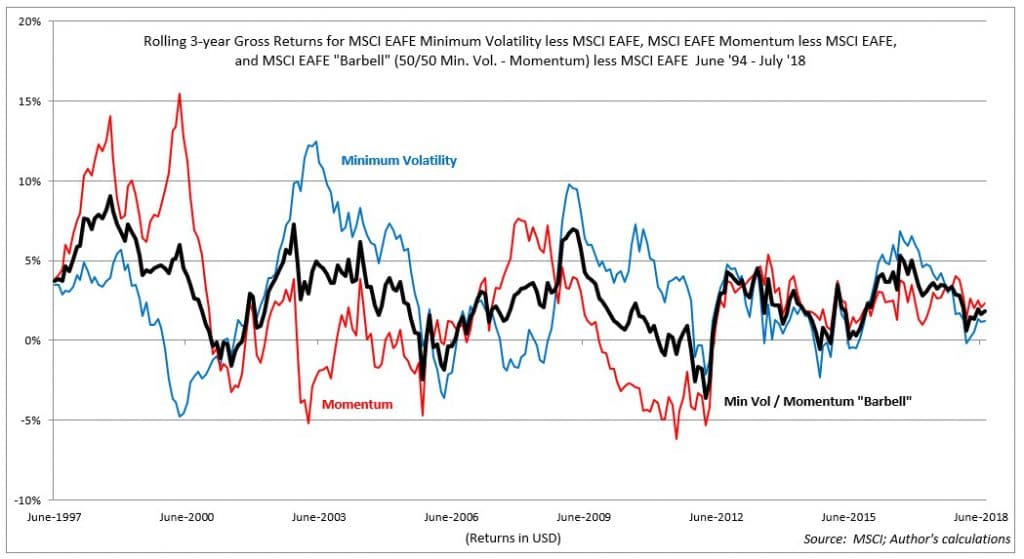

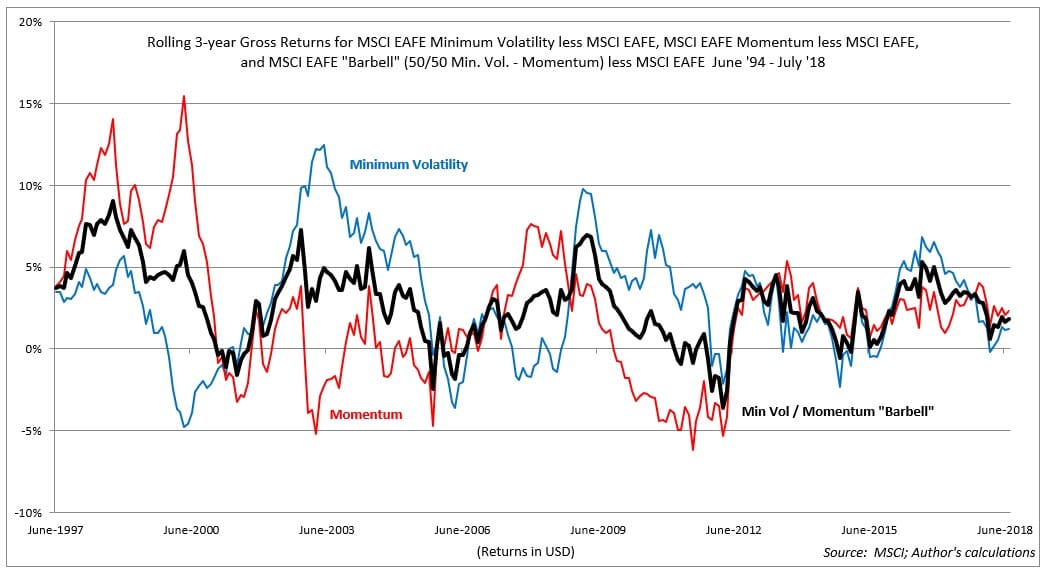

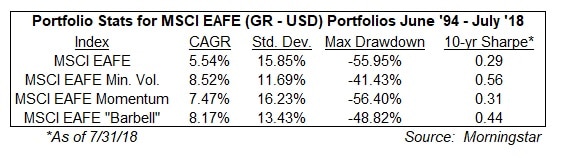

For the EAFE universe, both minimum volatility and momentum have handily outperformed the EAFE index itself by a significant margin over the last twenty-four years, but, as was the case in the U.S., there were significant periods of underperformance for each strategy. Even though the “barbell” portfolio was the second-best performer overall (see table below for full results), the approach suffered less frequent, shallower, and shorter periods of underperformance than did either strategy individually:

Similarly, the barbell strategy lagged only minimum volatility in terms of shallow and short drawdowns:

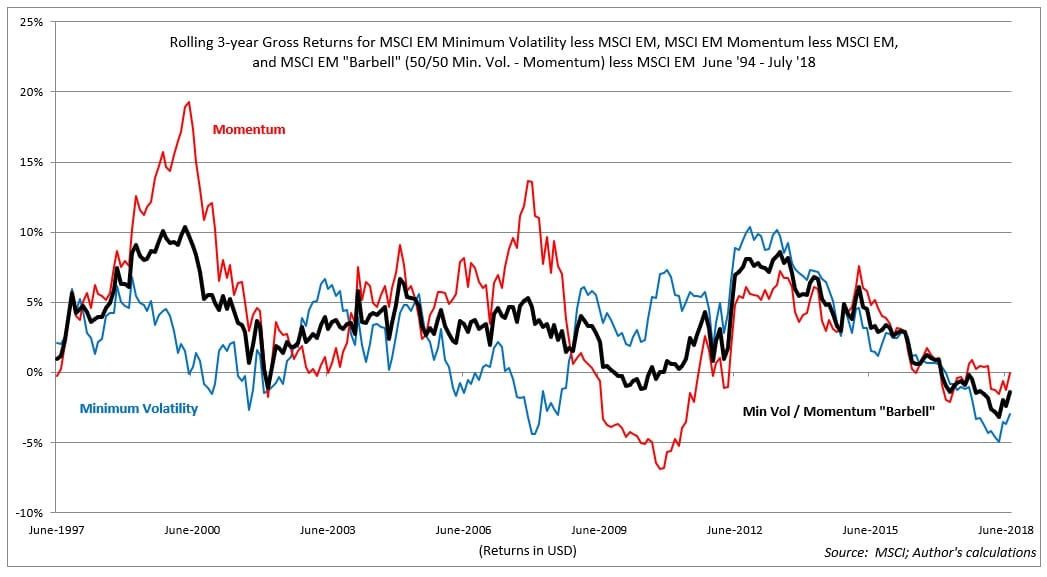

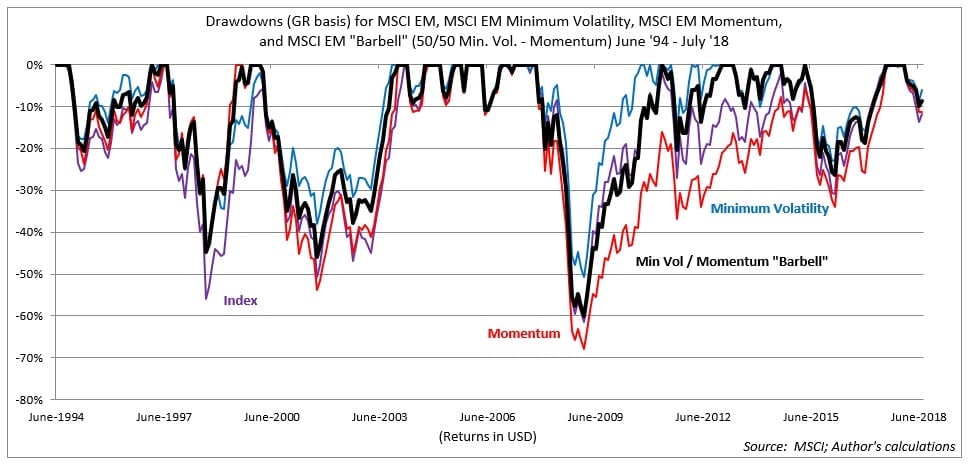

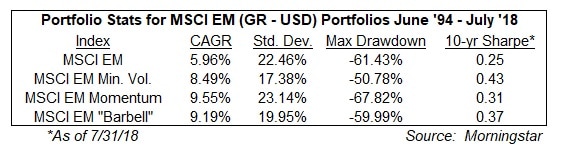

In the emerging markets sphere, the results were largely similar, with the barbell approach this time lagging momentum in terms of absolute returns, but providing a much smoother experience overall…

…with similarly favorable drawdown characteristics:

Here below are the portfolio statistics for the various strategies in both EAFE…

…and in EM:

Regular readers of my blog know that I am a staunch proponent of minimum volatility investing, and there are low-cost ETFs that can very readily provide this exposure to investors who desire it. Personally, I think this is a fine default choice if one portfolio has to be chosen over others. However, for investors who wish to balance that approach with something like momentum, the barbell approach does seem to have significant merit not just in the U.S., but also in foreign markets. Ideally, the barbell approach would be adopted by investors in non-taxable accounts which would shield the barbell from the deleterious tax effects of rebalancing.