In a previous post, I discussed how equal-weighting the positions in an equity portfolio historically has yielded greater returns than portfolios composed by market capitalization. Among the reasons for this, I noted, were the benefits of implicit rebalancing, a tilt toward value, and a greater exposure to what is called the “small company premium,” which, simply put, is exposure to the excess returns historically generated by smaller firms.

The tradeoffs presented by an equal-weighted portfolio can clearly be seen by comparing the S&P 500, which is an index weighted by capitalization, versus its equal-weighted version. Going back to 1990, the S&P 500 equal-weighted portfolio has generated annualized returns of 11.2%, versus just 9.64% for the capitalization-weighted S&P 500. On the other hand, the equal-weighted portfolio has had slightly higher volatility with a standard deviation of roughly 16% and a maximum drawdown of about 55%, versus 14% and 51%, respectively, for the cap-weighted index.

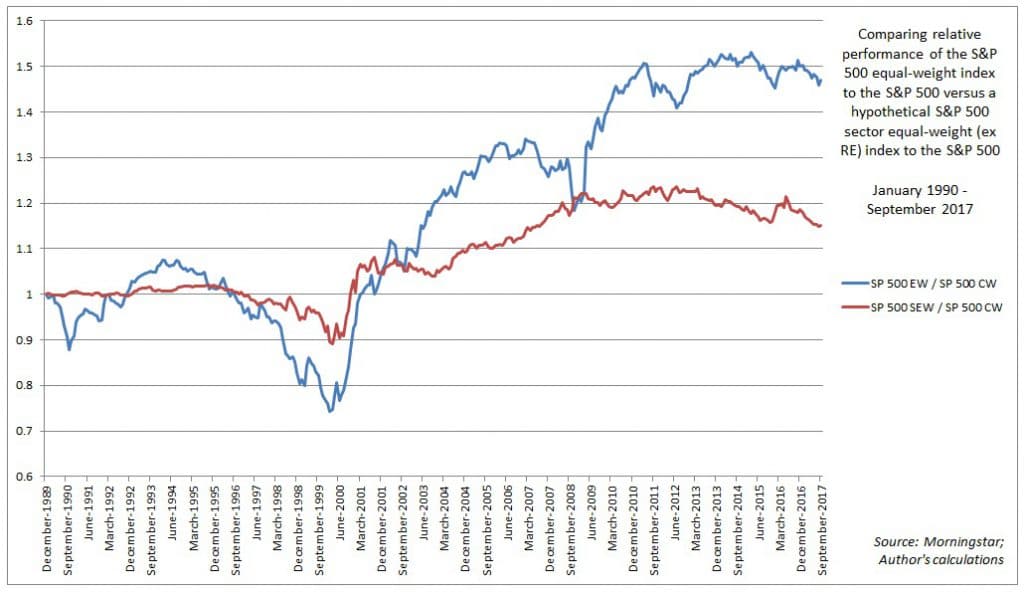

However, I wondered if there might be more of an advantage to equal-weighting than just tilts toward value and small size. Given that the change toward market capitalization weighting has somewhat altered the index’s balance, leaving it vulnerable to major shifts toward the largest companies in the hottest sectors during cycles like the tech bubble, I thought perhaps that the implicit rebalancing of an equal-weighted portfolio might avoid these distortions. To some extent, this is true: the largest sector weighting in the S&P 500 equal-weight index is about 16% (consumer discretionary), whereas the largest sector weighting in the cap-weighted index is 23% (information technology). Yet further analysis reveals that while less exposure to hot sectors might be an advantage to equal-weighting, there is still a wide gap between an equal-weighted index and a hypothetical index equally weighted by sector [Note: for this illustration, real estate was excluded as it was only recently awarded its own sector weight within the parent index.]:

If sector balance is not a factor in equal-weighting, can the implicit rebalancing still perhaps yield more consistent returns?

To test this idea further, I created distribution tables for rolling three-year returns for both the equal-weight and cap-weighted indices. From January of 1990 through September, the S&P 500 equal-weighted index yielded positive results 88% of the time:

This compares favorably to the cap-weighted S&P 500 index, with positive outcomes just 80% of the time:

Even though the equal-weighted index generated positive results more consistently with a narrower range of outcomes, the results are not significantly different between the two distributions to conclude too much from them.

Given this, I wondered if another index more broadly composed and with a longer history might yield more conclusive results. To that end, I performed the same test on the Russell 3000 index and an equal-weighted version of it. The results of this test were very similar in that the equal-weighted version yielded positive results more often and with a narrower range of outcomes, but, again, the differences were not significant enough to conclude anything substantive:

In sum, there are many advantages to an equal-weighted equity portfolio versus a generic cap-weighted portfolio, but more balanced sector exposure, at least domestically, is not one of them, and a greater consistency of returns is only a slight advantage at best.