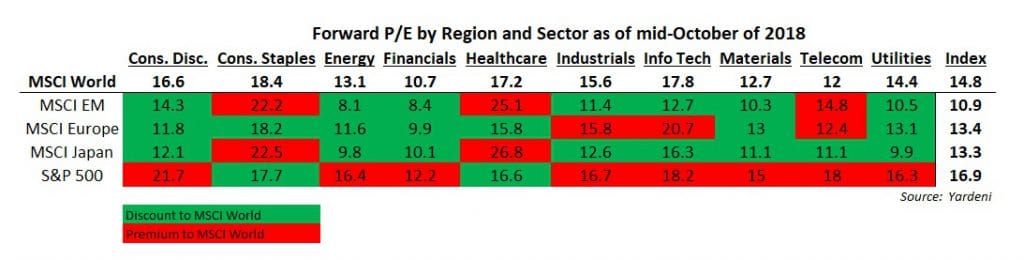

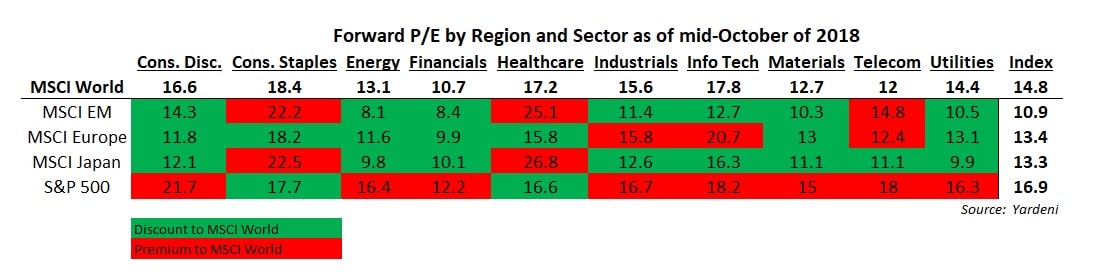

Given the recent turmoil in global equity markets I thought it would be interesting to check in on global equity valuations to determine if any bargains currently exist. Data from Dr. Ed Yardeni show that the U.S., in aggregate, is currently trading at a premium to global stocks of all kinds, though when broken down by sector, valuations vary a bit:

For example, emerging markets appear to be the cheapest basket in the global equity market, but emerging market healthcare and consumer staples stocks are among the most expensive among their global peers. Interestingly, this is also true for Japan, despite it being the world’s second cheapest market in aggregate. In both EM and Japan, tech stocks appear to be bargains compared to their European and U.S. counterparts.

Now, it should be no surprise that industries such as telecommunications and utilities are more closely tied to the fortunes of their local economies; after all, they are largely immobile in their geographic footprint, and domestic sales account for close to 100% of their revenues. For global industries such as technology and healthcare, however, investors should be aware that sometimes these foreign sectors trade very differently from market to market.

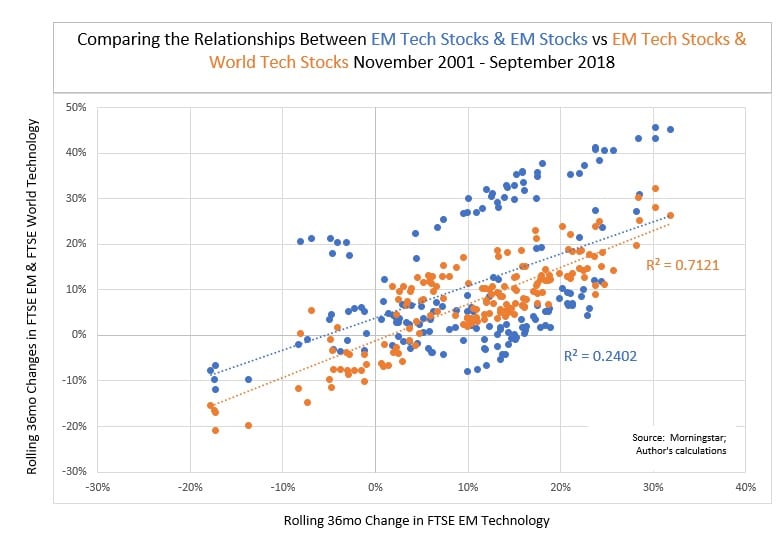

For example, investors intrigued by the apparent cheapness of both Japanese and emerging market tech stocks might think they are making a bet on cheap tech stocks poised to benefit from the global tech boom. This has largely been the case in emerging markets, where tech stocks have traded more in-line with global technology shares than with the local equity markets:

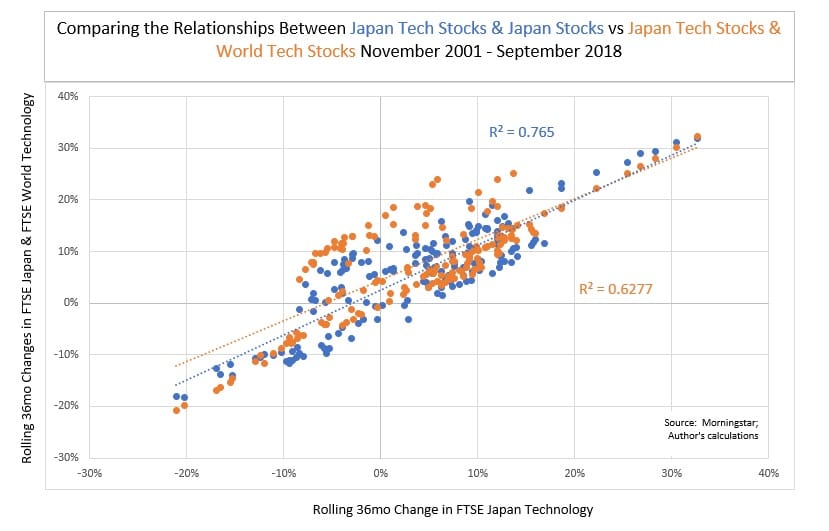

In Japan, however, tech stocks have been tied more closely to the fortunes of the general Japanese market than to global technology shares:

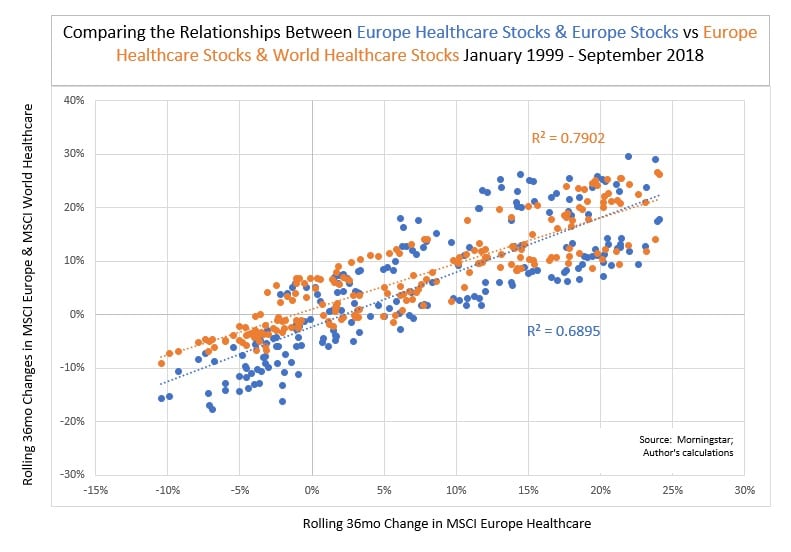

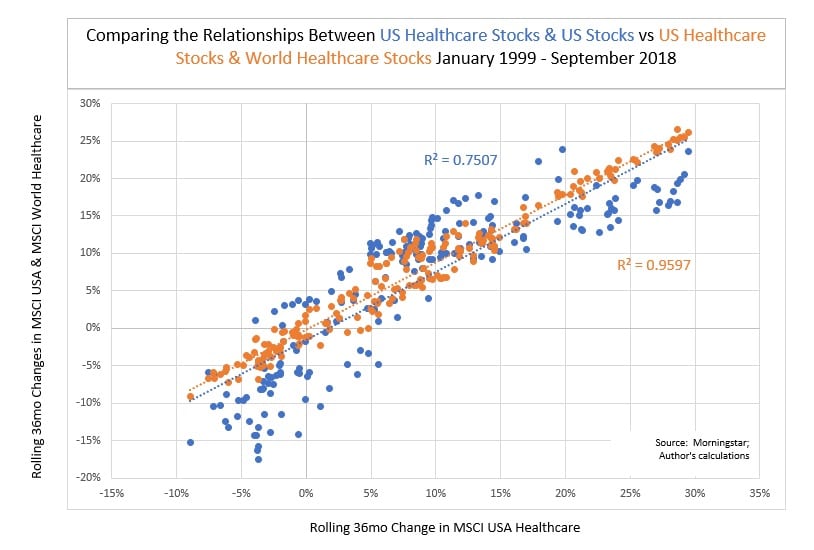

In the healthcare space, both Europe and the U.S. trade at discounts to the global healthcare sector. It is interesting to note that in each case, healthcare stocks were more closely aligned with global healthcare stocks than with the local markets:

When investors go abroad to look for bargains, it is important that they understand that relationships vary between regions, and even between regions and component sectors. Unwary investors who, when placing their bets, fail to look past the veneer of aggregate valuations, and who fail to appreciate the different dynamics of various global markets, can end up with unintentional bets, and, of course, unpleasant surprises at times.

Note: All returns are in USD

Links to Ed Yardeni’s source materials: