Global equities are more alike than most investors might realize, and this is readily revealed when comparing equities at more basic levels, whether it be at the sector, industry, or even the individual company level. Given that, it is instructive to see that no matter what the market, some industries are universal outperformers, meaning they tend to do much better than their respective broader universes, while others are the opposite, and lag their parent markets considerably.

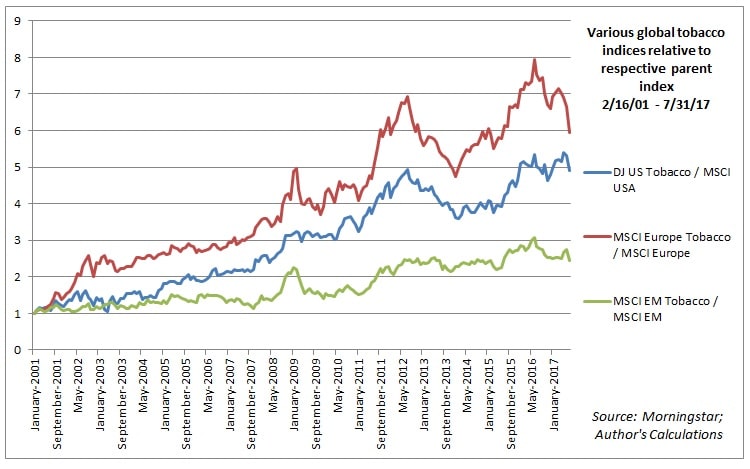

A good example of an industry that has outperformed the broader equity market no matter what region is tobacco. Going back to February of 2001 (the earliest common date), tobacco stocks have delivered index-crushing returns in emerging markets, the U.S., and, most spectacularly, in Europe:

This probably should not be a surprise. After all, the dynamics for tobacco are the same worldwide: the major markets are dominated by a few major players which enjoy wide moats, the results of which are stable market share and steady, elevated profit margins. Tobacco stocks tend to trade at a premium to the broader market because of these reasons, but that may not mean they are ‘expensive’ in the traditional sense of the word. Consider that during the 2007-2009 global recession, tobacco profits fell 10%, with the decline lasting only six months, whereas earnings for the entire market fell 42%, and took six years to recover, according to Morgan Stanley. Such statistics perhaps explain not only the outperformance of tobacco stocks, but also why investors are willing to pay up for them.

Conversely, the airline industry has been universally a dog, with airline stocks significantly underperforming the broader market in the U.S., Europe, and in emerging markets:

Airline stocks of all kinds seem to suffer from the afflictions of high fixed-costs, intense competition (which hurts margins and profits), terrorism concerns, and periodic bouts of rising fuel costs, among many other things. It is no wonder, then, that the valuations of many airline stocks appear to be bargains. Investors who might be tempted by these compelling numbers would be wise to consider just why airline stocks are so cheap in the first place.

Not all industries a that black and white, however. A few industries have enjoyed success mostly in the U.S., and, conversely, some industries that in the U.S. have been huge failures have enjoyed great success outside the U.S. An example of the former is the road & rail industry, which has crushed the broader market in the U.S., but has lagged both in Europe and in emerging markets:

Perhaps a good explanation for this is that the railroads in the U.S. are an oligopoly, meaning they, like tobacco companies, have wide moats, and have little to worry about in the way of competition from new players. For their cargoes, railroad pricing is generally dictated by contract, so their revenues tend to be fairly stable even during rough periods. In contrast, the European railroad market is more fragmented, with far more players than in the U.S. Additionally, most foreign rail operators are subject to a much higher degree of regulationthan their American counterparts.

Automobile stocks, on the other hand, have fared very well in Europe and in emerging markets, while they have been terrible investments in the U.S.:

There are perhaps many reasons for this divergence in performance. American automobile manufacturers suffer from a much higher cost structure than their foreign counterparts as they generally employ union labor to produce their vehicles, and a consequence of that is very steep costs for things such as employee healthcare. This is not true in many European countries which utilize government-run healthcare, thus reducing this direct expense for the manufacturer (I say “reduced” as it is a certainty that the cost is merely deflected into higher taxes of some kind). Furthermore, American brands suffer from doubts about their reliability, and their sales aside from things such as trucks and SUVs have been poor even in their home market. As most readers will recall, only Ford among American manufacturers was not bailed out by the federal government during the most recent global recession, and bitterness over this still has some impact on how consumer view the other domestic car companies.

In conclusion, prospective investors would be well-served not just to look at valuation metrics or purely domestic performance to gauge the profitability of a potential investment. There are many valuable lessons to be learned, for example, from studying a company’s or industry’s foreign counterparts as well. Such analysis may better reveal the true nature of an investment idea, and may even lead to superior ideas abroad.

Both the author and clients of Fortune Financial own shares of Ford.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.