In a previous articled titled, “Learning the Wrong Lessons,” I discussed how the small company premium is a real enough phenomenon, but that for it to be realized by investors, portfolios must be sufficiently diversified in order to reduce the extreme risk inherent in small companies. However, most studies on this subject have examined portfolios of large and small companies only on the basis of random selection, which does not tell us much other than that individual large companies tend to mirror the capitalization-weighted market more closely and with substantially less risk than individual small companies.

However, this leaves us a little short in terms of knowing how many small companies are needed in order to diversify sufficiently a portfolio of them, or whether there are pockets of the small company universe that may be less risky than others, etc. In order to test these ideas a little more, I wanted to compare the returns of U.S.-listed large and small companies within each sector to determine if the small company premium is easier to capture with pooled investments at the sector level, and also to get a general sense of which sectors have been responsible for the relative performance of small company portfolios.

First, however, I wanted once more to demonstrate the small company premium, which simply states that small companies tend to offer superior long-term returns both to large companies and to the broader market. This is easily seen in the twenty-five-plus years of returns captured by the relevant Dow Jones indices [Note: I am using Dow Jones index return data for this post as Dow Jones was the only provider with sector-level small- and large-cap returns]:

Since January of 1992 when common data for these Dow Jones indices begin, U.S. small companies returned 10.6% annually, while large companies returned 9.03%, which is a return premium of about 160 basis points. When compared to the U.S. market as a whole, which returned about 9.55%, the small company premium was still greater by more than 100 basis points.

Yet sector-level data, which are admittedly incomplete, reveal that the small-company premium was concentrated in only a few sectors; in fact, of the sectors observed, only four small-cap portfolios outperformed both generic domestic large caps as well the generic market-weighted index. Of those four, only three outperformed generic small caps as well:

Conversely, of the sector-level large cap portfolios, six outperformed the generic large cap portfolio, but only two, – healthcare and technology, – outperformed the broader index.

There are some simple explanations for this bifurcation in sector-level results. For example, the oil and gas sector is extremely cyclical as it closely tracks, obviously, the price of oil. When the oil price is increasing, smaller companies like “E&Ps” (“exploration & production”) are more likely to outperform larger, higher-quality companies like the integrated producers:

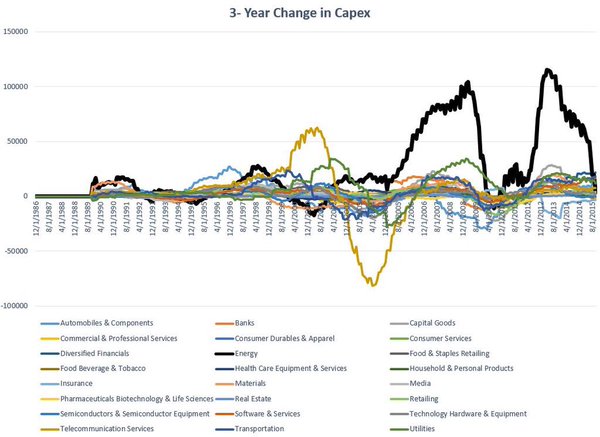

It goes without saying that the oil business is extremely cyclical, and prone to overinvestment during boom times, which means that many of these smaller companies will likely fail or dilute shareholders with secondary offerings to pay down debt accumulated during the boom. For an example of this excess, just look at this graphic on capital expenditures from my friend, Patrick O’Shaughnessy:

The peaks in energy capex coincided with the outperformance of small oil and gas companies as well as the price of oil.

The other line that stands out on Patrick’s chart is the telecommunications sector, which experienced a huge bubble in the late 1990s. The effects of this bubble bursting are still being felt today as large telecommunications companies have crushed their small counterparts in the years since:

In sum, many small companies fail because they start their life in the midst of a bubble, or at the very least, close to a peak in the economic fortunes of its industry. Therefore, in order to realize the fullest potential of small company investments, sufficient diversification is needed not just in terms of the aggregate number of small companies owned, but also in terms of broad representation across all of the various sectors and industries within the market. It is only in this way that the very real risks of owning small companies can be alleviated to a tolerable degree.

For further reading, see Alpha Architect’s Jack Vogel here, and myself, here.