The historical outperformance of companies that return capital to shareholders tax efficiently through buybacks is no mystery. It is, in fact, a well-documented and thoroughly analyzed phenomenon. However, there exists a tired but persistent narrative that says that CEOs who engage in buybacks are ‘out of ideas,’ and are content merely to cannibalize their future growth for “short-term” rewards. The corollary to that narrative is that investors would instead be better off investing in companies that focus on investing in the future via large capital expenditures, or “capex” spending.

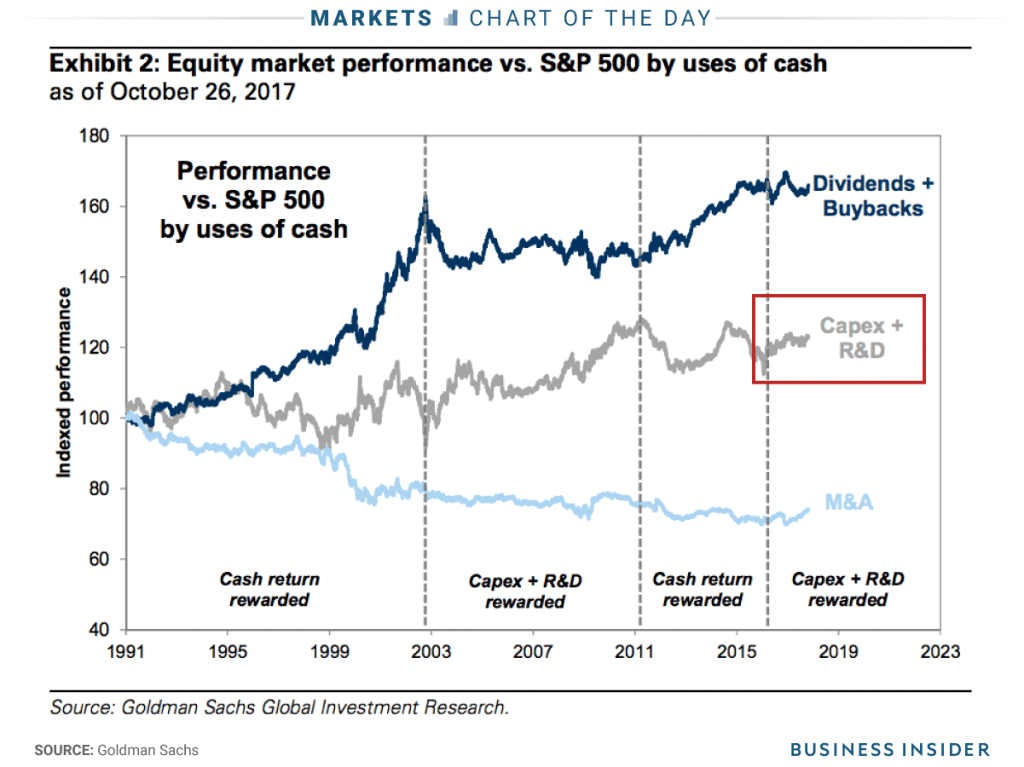

Supporting this narrative are data from Goldman Sachs, which seem to show that the market is cyclical in terms of how it rewards investors by alternately rewarding return of cash (via dividends and buybacks), and capital expenditures. Below is a graphic from Business Insider which shows how these cycles have played out over time:

On the face of it, the graphic is convincing, and an investor could reasonably conclude that the current cycle has turned in favor of capex-heavy companies. However, it would be incomplete to stop the analysis there. According to the graphic above, prior to the current ‘cycle,’ the last time capex-heavy companies outperformed was from roughly 2003-2011. A closer look at the data by sector reveals why.

From 2002 through 2010, which is roughly the period of prior capex dominance, the capex-heavy energy sector was far and away the best performing sector in the market, averaging an annualized return of 16%, versus less than 7% for the market as a whole:

Propelled by a weak dollar, the price of oil soared, and energy stocks reaped a rich reward. However, higher oil prices demand more exploration and more drilling, which of course means more capex spending, and it is therefore no surprise that the energy sector saw the greatest increase in capex spending over that period (table via Business Insider):

So while the historical composition of Goldman Sachs’s proprietary “capex” basket is unknown, it seems safe to assume that from 2003-2011 it was heavy in energy-related companies.

The other massive outlier in the table above is the consumer discretionary sector, which saw huge capital expenditures over the same period 2004 – 2008. This was in large part due to the housing bubble (home builders are part of the consumer discretionary sector). It is therefore reasonable to conclude that home builders, too, were featured within the capex basket during this time.