S&P’s Indexology blog recently published a great paper titled “Outperformance in Equal-Weight Indices.” In the paper, the authors looked at several different ways in which investors could create “barbell” strategies with various equity indices. For example, the authors demonstrated the usefulness of pairing the small company and value exposures offered by equal-weighting with a momentum strategy, as well as the utility of paring equal-weighting with low volatility.

I found the barbell idea very intriguing, but since the authors already explored in great detail the benefits of pairing certain factor strategies to equal-weighting, I wanted to see what the impact would be of matching up momentum with low volatility. The idea, of course, is that these two factors are on opposite ends of the spectrum, as momentum attempts to capture the full benefit of a strong trend, while low volatility is focused on avoiding excessive movements in one direction or the other. The benefits of pairing the two seem intuitive, as. for example, momentum’s vulnerability to a sharp reversal in a trend could be alleviated by matching it with low volatility.

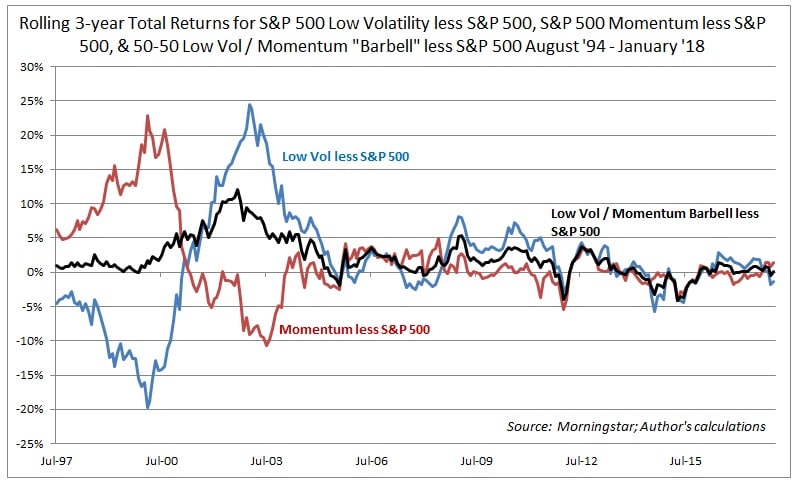

By subtracting the overall market’s (the S&P 500) return from both the momentum and low volatility strategies’, we can see when each strategy would have been both outperforming and underperforming. The biggest divergence between the two strategies was in the run up to and the aftermath of the peak of the tech bubble in 2000:

These wide divergences seem to suggest that a pairing of the two strategies would have yielded substantial benefits over the period observed. When comparing the two series to a 50-50 low volatility / momentum “barbell” (rebalanced annually), we can see that such a strategy would have captured a decent amount of the outperformance of each individual strategy without suffering as many periods of somewhat steep underperformance:

The pairing of the two strategies did not suffer from lackluster performance, either. From August 1994 through January of 2018, the barbell strategy averaged higher returns than the market, as well as both the low volatility and momentum strategies:

Interestingly, the strong performance of the low volatility / momentum barbell occurred even as the strategy suffered far shallower and shorter drawdowns than all but the low volatility index:

Obviously, these results are merely hypothetical, and past performance does not guarantee any future success. However, the results seem compelling enough to explore further, especially now that investors can access these strategies easily via low-cost ETFs that can be rebalanced simply and cheaply. Indeed, there are very few reasons not to consider barbell strategies such as this.

Addendum: Table of Returns and Portfolio Characteristics