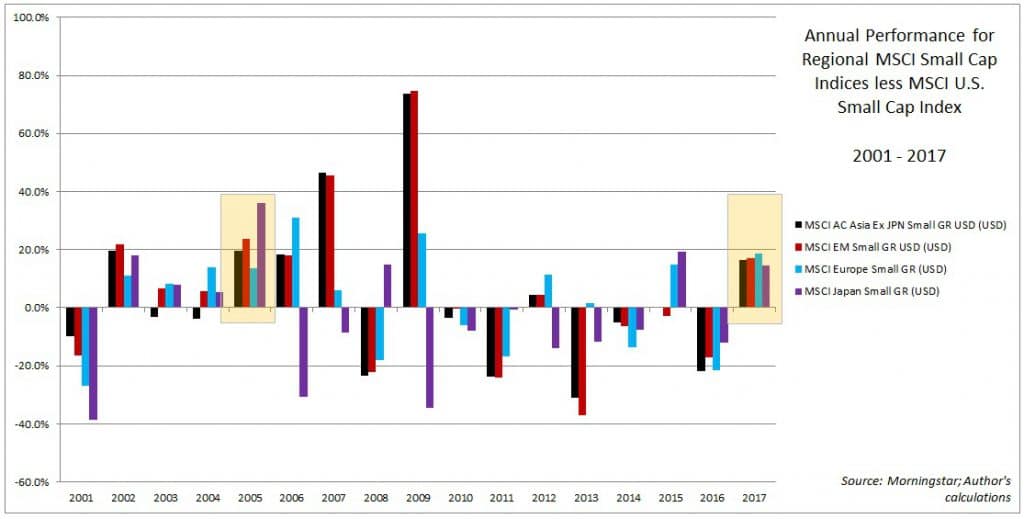

It has been widely-discussed that 2017 was the first year in quite some time that just about every major region outperformed the U.S. equity markets, at least when measured in dollar terms. What has been less discussed, however, is that global small cap stocks, – whether in Japan, Asia, Europe, or emerging markets, – outperformed small cap U.S. stocks by an even greater margin. In fact, you would have to go back to 2005 to see such strong and widespread performance for non-U.S. small caps relative to U.S. small caps:

(Note: right-click and select “open image in new tab” to enlarge)

The performance of small cap stocks are typically more closely aligned with their parent economies, and given that last year was a breakout year of sorts for the global economy, the strong performance of small cap stocks worldwide should not be surprising. Furthermore, as we discussed last May, foreign small cap stocks have the advantage of being far more diversified across sectors and industries than their large cap counterparts, so, in aggregate, they offer investors more balanced exposure to the parent economies.

Another key advantage to broader sector and industry exposure is that the relative cheapness of foreign small caps relative to U.S. small caps is less a product of aggregation bias, and therefore more likely indicative of real, versus merely apparent, value. It is important to note that despite 2017’s surge in global small cap stocks, all major regions still boast higher dividend yields and lower earnings multiples than U.S. small caps:

Finally, foreign small cap stocks have offered investors better diversification benefits than foreign large caps, which is critical in a time of somewhat elevated correlations across the globe. As the global economy continues to improve, a combination of an improved earnings outlook and favorable valuations should continue to boost the case for exposure to foreign small caps.