As an adviser who allocates a large portion of client assets to low-cost index-type ETFs, and who manages a fair amount of my own portfolio in this manner, I believe that the trend toward lower-cost index-type investing, – I hesitate to call it “passive” investing, – is generally a welcome one. I say this because research has shown that lower-cost funds exhibit much lower “behavior gaps” than higher-cost alternatives, which means that investors seemingly are moving in the right direction as far as improving their dreadful record when it comes to investment performance.

That being said, I do think that, like anything else, there are correct and incorrect arguments being made in favor of index funds. Before I go further, I want to be clear that when I speak of index funds, I am referring to the garden-variety market-capitalization weighted funds such as those which track the S&P 500 index, or, for foreign equities, the MSCI Europe, Australasia, and Far East (or “EAFE”) index. These seem to be among the most popular, and, though I haven’t the data to support it, I would assume they are also the leaders, by far, in terms of assets under management.

So, to begin, I visited the website of indexing advocate Vanguard Group, which is becoming the colossus of asset management. On their site, they have a page dedicated to the advantages of indexing, and here a few they list:

- Low expense ratios

- Tax efficiency

- Risk control

- Diversification

With net expense ratios for many index funds relentlessly pushing toward zero, there really is no argument that cheap market exposure is a definite positive for index investing. Short of some sort of

DRIP (“dividend reinvestment plan”) plans, which may not charge investors for participation, index funds are probably the closest one can come to investing for free. I think that this cost advantage is the primary driver of fund flows to index managers. I think that Dr. Ed Yardeni summed up this trend well when he wrote that investors are “

seeking out low-cost funds rather than cheap stocks.”

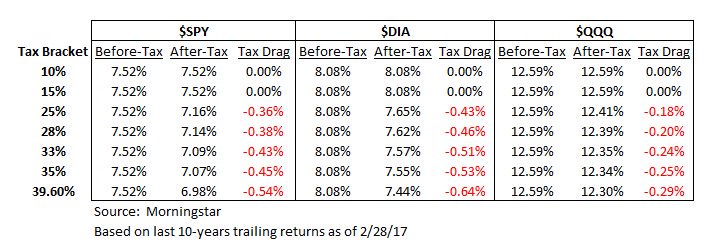

It is worth noting, however, that they are not the most efficient choice. I ran the numbers on three of the most popular index-based ETFs, and I was surprised how high the tax drag can be on even the low-cost, low-turnover index-tracking ETFs:

In this illustration, the assumption is for long-term (meaning longer than one year) holdings, and, for simplicity’s sake, a married couple filing jointly. In the United States, qualified dividends and long-term capital gains are not taxed for investors in the 15% marginal bracket and below, so that explains the null tax drag.

However, for those in the highest bracket, the annual tax drag can start to approach one-half of one percent annually for the S&P 500 ETF ($SPY), and for the Dow Jones ETF ($DIA), presumably due to their higher dividend yield than $QQQ, which tracks the tech-heavy Nasdaq 100.

For tax-conscious investors,

tax-efficient allocation is paramount. Investors subject to the higher tax rates on dividends and capital gains should make the effort to allocate accordingly. For example, assuming non-dividend paying growth stocks are also owned within a given portfolio, it would make sense to own those in a taxable account, leaving the tax shelter of qualified accounts for the higher-yielding index funds. Unfortunately, in a graduated tax regime such as that which prevails today, it may be convenient to embrace a passive investing ideology, but it is likely to your benefit to be more active in terms of the taxable aspect of your allocation.

When it comes to “risk control,” Vanguard writes that “[i]ndexing eliminates the risk that an active manager will select securities that underperform the market. This is especially true with strategies that target broad-market exposure.”

This argument, in all honesty, seems a bit of a stretch. Sure, there is plenty of literature and research that attempt to demonstrate the futility of picking stocks, and so the logical conclusion is seemingly to own all the stocks, and to let the market sort it out over the long run. This would be a good idea except that the committees that populate their indices are oftentimes no better at stock picking than much-maligned active fund managers. There is real potential that the more choosing they have to do, the less effective indexing could become.

But churn in the S&P 500 is approaching such a pace that if it were to continue at this rate,

roughly half of the S&P 500 components will be turned over in the coming decade. In fact, turnover within the index has become so frequent that it opens up index investors to the very real possibility that they are sometimes throwing out the good for the bad. This was one of the conclusions of Professor Jeremy Siegel and Jeremy Schwartz who, in a 2004 paper*, noted that the original S&P 500 components (the index was established in 1957) actually outperformed the index itself, and with less risk.

Because the S&P 500 is weighted by market capitalization, it runs the risk of adding large but expensive firms at the wrong time, which, Siegel and Schwartz note, is exactly what happened during the tech bubble of the 1990s, when large components such as Qwest and WorldCom were added to the index, only to lose 65% and 98% of their respective values subsequently. Conversely, the unloved S&P 500 utilities index, which had shrunk to only about 3% of the index composition at the peak of the tech bubble, has been one of the top performers since, outpacing both the technology index, and the S&P 500 itself. Sometimes, the market can be very wrong with its assessment of future corporate prospects, and index-only investors would be wise to heed the warnings of the past.

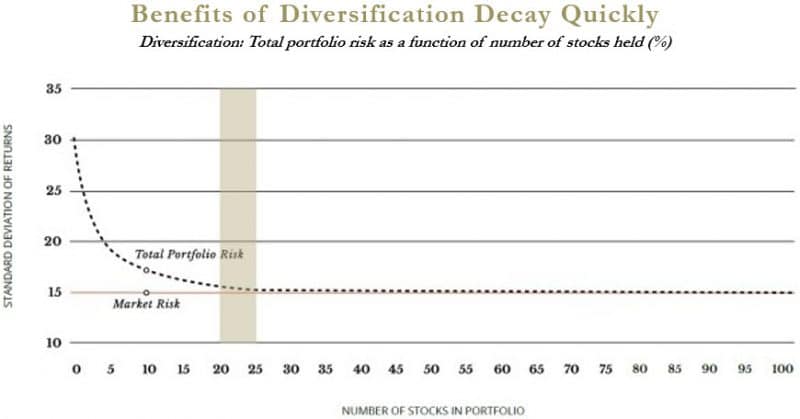

Finally, regarding diversification, Vanguard argues that indexing insulates investors against the risks of owning too few stocks, or too narrow segments of the market. I’ll concede the point that owning a pool of stocks is less risky than owning a handful of individual stocks, but it is highly debatable that index funds give you sufficient diversification. For starters, I have already noted that the

S&P 500 already has a huge correlation with technology stocks, so index-only investors are basically staking their futures on the prospects of American technology firms continuing to dominate and grow.

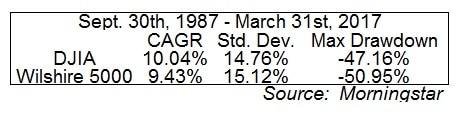

The idea that a pool of hundreds of stocks is necessarily less risky than a pool of far fewer stocks makes sense intuitively, but it actually is not always true. For example, the Dow Jones Industrial Average, – which is, admittedly, oddly constructed, – has outperformed with less volatility and with less of a drawdown than the Wilshire 5000 index, which I use here as it comes closest to being a proxy for the total stock market:

Obviously, there are many factors in play here: less volatile large cap stocks in the Dow versus thousands of small- and mid-cap stocks in the Wilshire; a large “quality” factor in the Dow, etc. Fair enough. So here are a few more examples: both the utilities and consumer staples subindices have far fewer components than the broader market, yet both have exhibited far less volatility. So, the fact remains: more stocks do not necessarily translate into more diversification and less volatility. Indeed, truly effective diversification means exposure to different factors, sectors, and other variables that, unfortunately, may not always be provided by a generic index fund.

I have neglected the foreign indices from scrutiny, but the arguments are very similar. They are likely the cheapest way to gain exposure to markets overseas, and I would assume they are also more tax-efficient than most active funds. Yet caveat emptor may be arguably more important than for investors in U.S. index funds. For example, heavy exposure to financials, which are always subject to heavy regulation, is one reason investors may want to deviate their foreign equities away from the index (by which I mean, as mentioned above, the EAFE), and look at opportunities in less-represented sectors. There may be a reason to own Italian or Spanish banks, but I have yet to find it.

In sum, there are many virtues to index investing, yet I feel as though their success is less a confirmation of their inherent virtues than it is an indictment of the fund industry which, despite inestimable sums and world-class talent, cannot offer a superior product despite what seems to me to be a great opportunity to do so. Index funds are far from perfect portfolios as the indices themselves are far from perfect. Better-composed indices such as equal-weight by sector, or, in the case of foreign equities, equal-weight by country would be improvements, in my opinion. Yet absent better choices (as is the case in most of the defined contribution plans I’ve seen), they are a reasonable default option for most investors. I would caution investors, however, that the work does not stop with buying an index fund. On the contrary, to maximize their utility, you should focus on some of their weaknesses, and seek to complement them with advantageous allocation decisions such as attempting to maximize their after-tax returns, and bolstering their performance by addressing their inherent composition weakness.

*”The Long-term Returns on the Original S&P 500 Firms,” by Jeremy J. Siegel and Jeremy D. Schwartz, The Wharton School, University of Pennsylvania, 2004.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.