First popularized as an investing concept by Warren Buffett, an economic moat is not much more than an advantage of some kind that allows a company to maintain and grow its position within an industry, thus ensuring healthy profitability. The importance of a moat cannot be understated. In fact, much of Buffett’s success as an investor can largely be attributed to buying companies with wide moats, and avoiding those with narrow moats, which he has characterized as “too risky.”

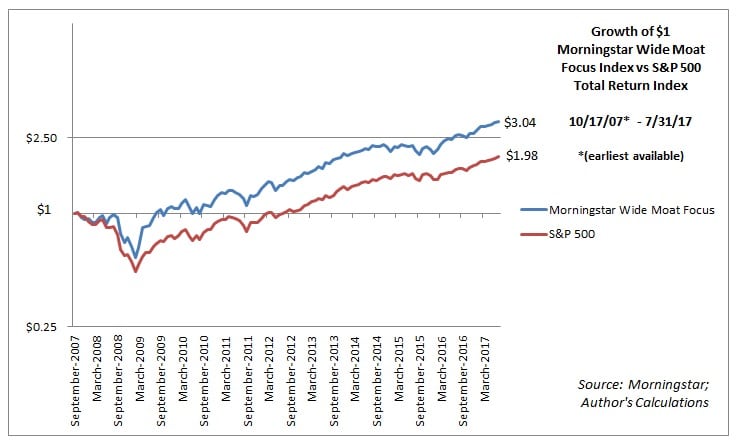

Following Buffett’s lead, Morningstar has created various indices based on specific criteria such as “switching costs” (e.g. inconveniences experienced when changing vendors), and “cost advantage” (think Wal-Mart) that allow certain companies to outperform the competition. This kind of combined quantitative and qualitative approach allows for a simple assessment of a company’s moat. The wisdom of focusing on wide moats is apparent when viewing the evidence as wide moat stocks have generally outperformed the broader market…

…oftentimes with shallower drawdowns:

The purpose of this post, however, is not to repeat what others have said quite well regarding moats. For more on the general topic of moats, please consult the following resources:

Morningstar’s What Makes a Moat?

Patrick O’Shaughnessy’s interview with Pat Dorsey, who focuses his investment firm on wide moat companies:

Pat Dorsey’s presentation on moats, Moats and Macro

Ensemble Capital’s The Death (of Many) Brands

Buffett on Economic Moats – Alpha Architect

Now that that is out of the way, I will return to the focus of my post, which is to identify and assess what firms or industries generally have not just the widest, but, more importantly, the most lasting moats. The reason I think a lasting moat is important to consider is because history is full of examples of wide-moat companies that were disrupted by new entrants (think Apple upending Nokia), or new technologies that not only narrowed the moats, but shattered the companies (think digital photography crushing Kodak). It goes without saying that no moat is invulnerable, but I do think that certain industries and companies do enjoy something close to permanent moats, perhaps because their products and services are less likely to be substituted for, or because geography or regulation have made them pseudo-monopolies.

Here are a few of the industries and companies that I think might enjoy lasting moats:

Railroads – At one point, railroads were the largest single industry within the stock market, constituting something like two-thirds of the stock market circa 1900. When automobiles and airplanes threatened to destroy the moat enjoyed by railroads, railroad stocks became depressed until it became apparent that railroads were still the most efficient method of transporting commodities and materials long distances across the continent. The industry went through a period of consolidation, with a handful of companies competing with each other by region. Eventually, the advantages enjoyed by the railroad industry propelled it to strong returns that surpassed the market. There are certainly threats to the railroad business as more oil may eventually be shipped by pipeline than by rail, and the decline in uses of things like coal may depress rail traffic significantly. However, until a more efficient and cost-effective method of transporting vast quantities of materials across wide distances is developed, railroads should continue to enjoy a lasting moat.

Tobacco – It is no surprise to long-time readers that I consider tobacco to be one of the most compelling long-term investment opportunities available. For one, tobacco use goes back hundreds of years, and has hardly evolved over that period, so it has tremendous staying power. While tobacco use is in decline domestically, internationally usage is still steady if not growing. Certain regulations like restrictions on advertising insulate incumbent tobacco companies from competition, which has resulted in the top four tobacco companies enjoying more than 90% of industry revenues. The obvious threats to tobacco are regulatory, but it seems unlikely that governments, which tax the product heavily, would ever move to ban the products as the failure of alcohol prohibition demonstrates the folly of such a ban. For these reasons, it is difficult to imagine the moat enjoyed by the tobacco companies being narrowed in the foreseeable future.

Airports – Airports constitute one of the few investment opportunities that abound outside the U.S., but are nonexistent within the U.S. As discussed previously, publicly traded airports from France to New Zealand have generated market-beating returns, even when, in the case of Mexico, the market in general has been terrible. Their moats are obvious: they have next to no competition in their areas of operation, and thus they have tremendous pricing power. In fact, airports seem to combine the best of what gives railroads a wide moat, – geographical and logistical dominance, – with the regulatory-induced insulation against competition enjoyed by tobacco. Valuations for many airport stocks are high, and the best may already be priced in, but their moats seem to have little chance of being breached.

It is important to note that continued wide moats may not necessarily equal out-sized returns for these industries, but it should theoretically give them a better chance of not disappointing investors. The key point to moat investing, I believe, is not just to look at what success has allowed a company to create and benefit from its moat, but also to consider whether that moat is sustainable in a period of increased dynamism when new technologies can shrink a well-established moat in considerably less time than it took build it.

Additional Graphic: Return and risk characteristics for S&P 500 and Morningstar Wide Moat Focus Index 10/17/07 – 7/31/17:

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.