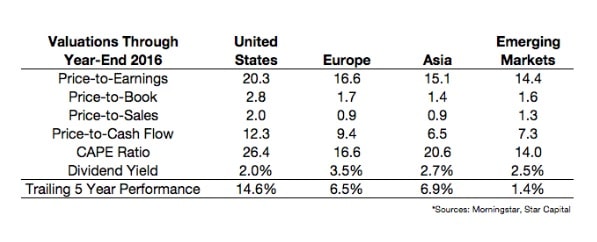

In his inaugural Bloomerg View column, Ben Carlson discussed the valuation differences among the various equity markets around the world:

Not only do emerging markets appear considerably cheaper than US stocks (particularly on a CAPE basis), there is a case to be made that the most recent period of relative US outperformance vs emerging markets (or EMs) – the longest since the 1990s – is a bit long in the tooth:

Source: Morningstar

However, investors who are tempted to abandon ‘expensive’ US markets and go all-in with ‘cheap’ emerging markets should consider first just what the proper role of emerging market equities is in a portfolio. In my opinion, emerging markets are not core portfolio holdings. This is because they are extremely vulnerable to political turmoil, and currency instability. As JP Morgan’s chief emerging market strategist, Richard Titherington, puts it, many of the world’s emerging markets such as Russia and Brazil are actually very old nations, but they are still ’emerging’ because their economies and markets have been battered by ‘revolution and inflation.’

To illustrate Mr. Titherington’s point about emerging market susceptibility to revolution and inflation, he provides a great graphic that shows the frequent epochs of each in the recent histories of several prominent emerging markets:

Some might argue, though, that the world is a much different place from what it was in the 20th century. As much as we might like this to be true, it simply isn’t. As the Cato Institute recently noted, many of the countries on the list above are also among the highest-ranked (or lowest, depending on how one looks at it) economies when it comes to the ‘Misery Index,’ or inflation plus unemployment:

To illustrate further my point, it may be helpful to consider the case of Russia in isolation. Russia, by almost all measures is a ‘cheap’ market. At 5.9, it currently boasts the lowest CAPE ratio in Star Capital’s fantastic database. But Russia is cheap for a reason. The economy is currently under sanctions because of its actions in Ukraine, and inflation has been extremely high. Furthermore, with an autocratic government under Vladimir Putin, investors can never feel really safe putting their capital in Russia, given the risk of nationalization.

However, with such a low CAPE ratio, are all those myriad fears appropriately priced into Russian equities?

To answer that, would-be investors in Russia should understand that Russia is essentially a bet on oil prices. Consider the relationship between the FTSE Russia All-Cap Index (left axis) and oil (right axis) since:

Sources: Morningstar; FRED

Furthermore, Russian equities are extremely volatile – since data begin in 2002, the standard deviation of the FTSE Russia All-Cap Index is 33%, with a max drawdown of 78% – and it is not clear that they are really that cheap when you consider, as Philosophical Economics pointed out, that high-quality US energy stocks such as Exxon-Mobil and Chevrontrade with CAPE ratios of 11.7 and 12.3, respectively.

For reasons such as these, to make a large bet on any single EM country is conceivably as risky as making a large bet on any individual stock. Bearish investors like to chide their bullish counterparts for saying ‘this time is different’ when it comes to higher-than-average valuations in the US. However, emerging market bulls who insist that the long histories of inflation and political instability in EMs can safely be ignored are guilty of the same.

To be clear, I am not suggesting that emerging market equities have no place in an investor’s portfolio. I am simply arguing that because of their unique characteristics, they should be viewed more as diversifiers or satellite positions within a portfolio. But to expect emerging markets eventually to become diverse, prosperous, and stable markets like those in the US and Europe is probably misguided, and a foolish bet to make for investors with little room for error.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.