Over the last couples years there have been several articles (see here) and posts (see here) by bearish writers suggesting that market valuations must shrink as the Baby Boomer generation begins its forced distributions from retirement accounts. The theory is that the succeeding generations, being smaller than the Baby Boomers’, are not large enough to digest all of the shares the Boomers are selling, thus forcing down the value of shares.

Citing a 2011 report on the matter from the Federal Reserve Bank of San Francisco, Jesse Felder writes:

“[The researchers] found that demographics (specifically, the ratio between retirement age workers to peak earning and investing age ones) is responsible for 61% of the changes in the price-to-earnings ratio of the stock market over time…All this means is that there is a very strong relationship between the size of the generation that is currently in its peak earnings and investing years and the valuation of the stock market…It’s not magic; it’s simply supply and demand (mainly demand).” According to Mr. Felder, the greatest bubble in history (1981-2000) was directly correlated with the peak earning years of the Baby Boomer generation.

While it makes for an interesting theory, I’m afraid that the assertion stands the test of scrutiny.

For example, as Matt Klein of FTAlphaville pointed out, in 2014 the Fed researchers revisited the connection between equity valuations and demographic trends. What they found in this more expanded study is that of the G-7 nations for which data were examined, only in the United States did any sort of relationship hold between equity valuations and demographics. Given that equity ownership is a popular form of saving in most developed nations (although in some more than others), it seems strange that in only one market could a relationship be observed.

So what could possibly explain the anomaly of the United States equity market?

One possible explanation is that household ownership of equities is quite a bit higher than in other countries. Recent studies show about half of Americans own stocks, whereas in Germany, by contrast, only about 11% of households have equity ownership of any kind. Similarly, Japan, after a decades-long bear market, has relatively low levels of household equity ownership.

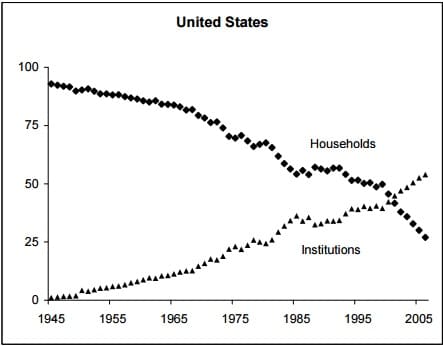

While that might be a simple explanation for the anomaly, the reality is that direct equity ownership by individuals and households in the United States, though high relative to other developed nations, has largely been in decline since the end of World War II, as University of Virginia researchers discovered.

As their chart demonstrates, household equity ownership has declined while institutional ownership has soared:

So, perhaps that explains it: even though individuals and households have reduced their outright equity holdings, they have not given up on stocks. Instead, they have outsourced their investing needs to institutions that act on their behalf. These institutions must have aggressively deployed their Baby Boomer cash and, as a result, have driven up valuations beyond their historical norm.

But a simple glance at the equity flows data destroys this notion as well. As Mr. Klein pointed out, more often than not, individuals and the financial institutions that serve them have largely been net sellers of shares. In fact, while Mr. Felder asserts that the “greatest bubble in history” coincided with the peak earning years of the Boomer generation, net equity purchases by households and financial institutions were almost always negative during that timeframe:

Note: Fed data found here

Given this, it seems odd to insist that somehow Baby Boomers were pushing up multiples while they were actually selling quite heavily almost all along.

The point of this post is not to pick on Mr. Felder; he himself mentions in his post that demographics are just one possible explanation for higher than average equity valuations over the last quarter century. But it seems to me that in order to be worth fretting over, the findings in the US would at least have to be confirmed by results in fellow Anglo-Saxon (that is, with a tradition of high equity ownership) countries like Canada and Great Britain. But, alas, they are not. What is more likely is that higher than average equity valuations have coincided with a 30+ year decline in interest rates, as well as a taming of inflation (thus making long-term investments like equities more valuable in present terms). Furthermore, as Ben Carlson wrote a few weeks ago, multiples could be higher (and thus future returns correspondingly lower) because the net return to investors is roughly equal today as it was in the past, the result of lower trading and holding costs. Finally, as Jesse Livermore of Philsophical Economics wrote last December, the tax-favored nature of equities is another boost to valuations.

The bottom line is that there are infinite reasons to worry about the stock market and future returns. Those worries should not be casually dismissed, but they must be put in context. Making major long-term investment decisions based on esoteric models is a surefire recipe for ensuring you will receive what you attempted to avoid in the first place, low returns.